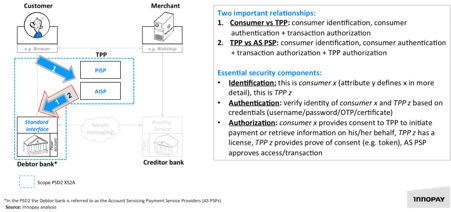

PSD2 –which is driving the change in January 2018– rules that the banks will have to open up their payment services to outside companies (Third Party Payment Service Providers – TPPs): payment initiation service providers (PISPs) on the one hand, and account information service providers (AISPs) on the other. Both services require authorization from the customers –whether private individuals or companies– and of course prior authentication.

The EU therefore seeks a payment market in Europe that is open to other actors in addition to the banks (fintech companies). In this scenario, managing users’ digital identities takes on a new dimension. This Discussion Paper from the EBA explores most of the risks and requirements of the new environment around the corner after the implementation of PSD2. It is evidently much more complex, and more sensitive. This is why APIs and the approach used to program them (open or closed application programming interfaces) is a matter for international debate.

Digital identity, a paramount asset

In the digital age, where mobile devices are now a tool for almost everything and all times, users’ data represent raw material of incalculable value. People registered with their username and password make financial transactions in real-time, associated to a first and last name, identity document, place of residence, gender, age and so on. Transactions associated to the retail sector, insurance, leisure… Not only do they provide information on expenditure, but also a record of customers’ revenues.

With the new PSD2, any company can become one of these TPPs and use the release of data to generate new income. There is no doubt that this is a race for the ownership of customers’ digital identities, and will involve hundreds of companies fighting for authorized access to this information. Europe considers it combines all the essential elements to deregulate the market and that the greatest beneficiaries will be the customers.

The components that guarantee a secure process are the following:

– Identification: definition of the attributes that confirm, beyond any shadow of a doubt, that the user is who they say they are and not someone different pretending to be them.

– Authentication: verification through credentials that the user is the customer they say they are (username and password, OTP, digital certificates and others).

– Authorization: the financial service providers (TPP) with a license to operate must be given authorization by the customers before they can access their accounts. They need to have proof of consent, which can be obtained through access tokens.

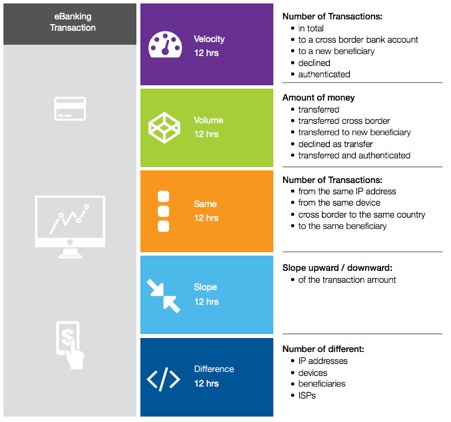

Risk-based authentication (RBA), a new ecosystem

Risk-based authentication (RBA) is the method whereby several levels of security are applied to the processes for authenticating customers or users to minimize the risk of violation. Some of the elements used in a risk-based authentication process are often the same as the ones used in some of the latest generation firewalls for classifying risk. These are:

– Role-based identification: the greater the privileges a specific user may have (for example a network administrator), the greater the risk controls they will be required to undergo. This is because they have an even greater capacity to break the protection.

– Location-based authentication: location is a key element for determining whether a transaction or bank operation entails risks or not. If the user or customer has logged on to an application or a financial service from a specific place and shortly after attempts to do the same thing from another totally different location, this may indicate an action that represents a risk to the bank and to the customers themselves.

– Activity-based identification: the characteristics of some financial transactions trigger greater levels of control. Transfers involving large sums of money, transactions between accounts in banks in different companies, sending money to accounts located in tax havens…

– Habitual behavior patterns: when a user makes a transaction that is not habitual in their behavior as a customer, that action is more delicate than the ones that follow their regular behavior patterns. These tend to be detected by measuring the speed of the linked transfers, the amounts of each transaction, and so on.

– Other important elements in the systems for RBA digital identity control include type of device, IP address, status of antivirus software, and others.

Businesses, from self-employed to SMEs and large companies, need financing solutions that suit their needs. Leasing is a method that can optimize the use of resources and which combines business liquidity (or lack of) with the use of assets. What is leasing and how does it work? Leasing is a financing method by which a […]

An API is a very useful mechanism that connects two pieces of software equipment to exchange messages or data in a standard format such as XML or JSON. Thus, it becomes an instrument that can be used to search for revenue, open the doors to talent or innovate and automate processes.

There are companies that collect and store bank data: information on accounts, transactions, credit-card operations, loans, investments... These companies' APIs give entities access to new markets and new customers.

Please, if you can't find it, check your spam folder

×

The email message with your ebook is on the way

We have sent you two messages. One with the requested ebook and one to confirm your email address and start receiving the newsletter and/or other commercial communications from BBVA API_Market

×

PROCESSING OF PERSONAL DATA

Who is the Data Controller of your personal data?

Banco Bilbao Vizcaya Argentaria, S.A. (“BBVA“) with registered address at Plaza de San Nicolás 4, 48005, Bilbao, España and Tax ID number A-48265169 . Email address: contact.bbvaapimarket@bbva.com

What for and why does BBVA use your personal data for?

For those activities among the following for which you give your consent by checking the corresponding box:

to receive newsletter from BBVA API_Market through electronic means;

to send you commercial communications, events and surveys relating to BBVA API_Market to the e-mail address you have provided.

For how long we will keep your data?

We will keep your data until you unsubscribe from receiving our newsletter or, if applicable, the commercial communications, events and surveys to which you have subscribed. Whether you unsubscribe or whether BBVA decides to end the service, your details will be deleted.

How can I unsubscribe to stop receiving newsletters and/or communications from BBVA API_Market?

You can unsubscribe at any time and without need to indicate any justification, by sending an email to the following address: contact.bbvaapimarket@bbva.com

To whom will we communicate your data?

We will not transfer your personal data to third parties, unless it is mandatory by a law or if you have previously agreed to do so.

What are your rights when you provide us with your information?

You will be able to consult your personal data included in BBVA files (access right)

You can modify your personal data when they are inaccurate (correction right)

You may request that your personal data not be processed (opposition right)

You may request your personal data be deleted (suppression right)

You can request a limitation on the processing of your data in the allowed cases (right of limitation of processing)

You will be able to receive, in electronic format, the personal data you have provided to us, as well as to transmit them to another entity (portability right)

You are responsible for the accuracy of the personal data you provide to BBVA and to keep them duly updated. If you believe that we have not processed your personal data in accordance with regulations, you can contact the Data Protection Officer of BBVA at the following address dpogrupobbva@bbva.com.

You can find more information in the “Personal Data Protection Policy” document on this website.

×

PROCESSING OF PERSONAL DATA

Who is the Data Controller of your personal data? Banco Bilbao Vizcaya Argentaria, S.A (“BBVA“), with registered address at Plaza de San Nicolás 4, 48005, Bilbao, España, and Tax ID No. A-48265169. Email address:contact.bbvaapimarket@bbva.com

What for and why does BBVA use your personal data for?

For the execution and management of your request, specifically, download the requested e-book/s.

BBVA informs you that, unless you indicate your opposition by sending an email to the following address: contact.bbvaapimarket@bbva.com, BBVA may send you commercial communications, surveys and events related to products and/or services of BBVA API Market through electronic means.

For how long we will keep your data?

We will keep your data as long as necessary for the management of your request, and to receive commercial communications, events and surveys. BBVA will keep your data until you unsubscribe to stop receiving our newsletters or, where appropriate, until the end of the service. Afterwards, we will destroy your data.

How can I unsubscribe to stop receiving newsletters and/or communications from BBVA API Market?

You can unsubscribe at any time and without need to indicate any justification, by sending an email to the following address: contact.bbvaapimarket@bbva.com

To whom will we communicate your data?

We will not transfer your personal data to third parties, unless it is mandatory by a law or if you have previously agreed to do so.

What are your rights when you provide us with your information?

You will be able to consult your personal data included in BBVA files (access right)

You can modify your personal data when they are inaccurate (correction right)

You may request that your personal data not be processed (opposition right)

You may request your personal data be deleted (suppression right)

You can request a limitation on the processing of your data in the allowed cases (right of limitation of processing)

You will be able to receive, in electronic format, the personal data you have provided to us, as well as to transmit them to another entity (portability right)

You can exercise before BBVA the aforementioned rights through the following address: contact.bbvaapimarket@bbva.com

You are responsible for the accuracy of the personal data you provide to BBVA and to keep them duly updated.

If you believe that we have not processed your personal data in accordance with the regulations, you can contact the Data Protection Officer at the following address: dpogrupobbva@bbva.com

You can find more information in the “Personal Data Protection Policy” document on this website.

Banco Bilbao Vizcaya Argentaria, S.A. owner of this portal uses cookies and/or similar technologies of its own and third parties for the purposes of personalization, analytics, behavioral advertising or advertising related to your preferences based on a profile prepared from your browsing habits (e.g. pages visited). If you wish to obtain more detailed information, consult our Cookies Policy.

Cookie settings panel

These are the advanced settings for first-party and third-party cookies. Here you can change the parameters that will affect your browsing experience on this website.

Technical Cookies (required)

These cookies are used to give you secure access to areas with personal information and to identify you when you log in.

Name

Owner

Duration

Description

gobp.lang

BBVA

1 month

Language preference

aceptarCookies

BBVA

1 year

Configuration Accepted Cookies

_abck

BBVA

1 year

Helps protect against malicious website attacks

bm_sz

BBVA

4 hours

Helps protect against malicious website attacks

ADRUM_BTs

Salesforce Marketing Cloud

Session

Required for monitoring of the service, inherent to SFMC

ADRUM_BT1

Salesforce Marketing Cloud

Session

Required for monitoring of the service, inherent to SFMC

ADRUM_BTa

Salesforce Marketing Cloud

Session

Required for monitoring of the service, inherent to SFMC

ADRUM_BT

Salesforce Marketing Cloud

Session

Required for monitoring of the service, inherent to SFMC

xt_0d95e

Salesforce Marketing Cloud

Session

Remember user preferences (if any)

__s9744cdb192d044faa1bf201d29fafd1e

Salesforce Marketing Cloud

Session

Remember user preferences (if any)

wpml_browser_redirect_test

WPML

Session

Text translation in the portal

wp-wpml_current_language

WPML

24 hours

Text translation in the portal

They are used to track the activity or number of visits anonymously. Thanks to them we can constantly improve your browsing experience

Your browsing experience is constantly improving.

With your selection, we cannot offer you a continuously improved browsing experience.

Name

Owner

Duration

Description

AMCV_***

Adobe Analytics

Session

Unique Visitor IDs used in Cloud Marketing solutions

AMCVS_***

Adobe Analytics

2 years

Unique Visitor IDs used in Cloud Marketing solutions

demdex (safari)

Adobe Analytics

180 days

Create and store unique and persistent identifiers

sessionID

Adobe Analytics

Session

Launch's internal cookie used to identify the user

gpv_URL

Adobe Analytics

Session

Adobe Analytics plugin: getPreviousValue Capture the value of a certain variable in the following page view, in this case the prop1

gpv_level1

Adobe Analytics

Session

Cookie used to store the DataLayer levl1 of the previous page.

gpv_pageIntent

Adobe Analytics

Session

Cookie used to store the pageIntent of the previous page.

gpv_pageName

Adobe Analytics

Session

Cookie used to store the pagename of the previous page.

aocs

Adobe Analytics

Session

Cookie that stores the first values collected at the beginning of a process.

TTC

Adobe Analytics

Session

Cookie used to store the time between the App Page Visit event and the App Completed event.

TTCL

Adobe Analytics

Session

Cookie used to store the time between the LogIn event and App Completed.

s_cc

Adobe Analytics

Session

Determine if cookies are active

s_hc

Adobe Analytics

Session

Cookie used by Adobe for analytical purposes

s_ht

Adobe Analytics

Session

Cookie used by Adobe for analytical purposes

s_nr

Adobe Analytics

2 years

Determine the number of user visits

s_ppv

Adobe Analytics

Permanent

Adobe Analytics plugin: getPercentPageViewed Determine what percentage of the page a user views

s_sq

Adobe Analytics

Session

ClickMap/ActivityMap features

s_tp

Adobe Analytics

Session

Cookie used by Adobe for analytical purposes

s_visit

Adobe Analytics

2 years

Cookie used by Adobe to know when a session has been started.

They allow the advertising shown to you to be customized and relevant to you. Thanks to these cookies, you will not see ads that you are not interested in.

The advertising is customized to you and your preferences.

Your choice means you will not see customized ads, only generic ones.

Name

Owner

Duration

Description

OT2

VersaTag

90 days

VersaTag Cookie used to store a user id and the number of user visits.

u2

VersaTag

90 days

VersaTag Cookie where the user ID is stored

TargetingInfo 2

MediaMind

1 year

Cookie that serves to assign a unique random number that generates MediaMind.

These cookies are related to general features such as the browser you use.

Your experience and content have been customized.

With your selection, we cannot offer you a continuously improved browsing experience.

Name

Owner

Duration

Description

mbox

Adobe Target

9 days

Cookie used by Adobe Target to test user experience customization.

×

Looks like you’re browsing from Mexico, so let’s show you the custom content for your

location. Change

Looks like you’re browsing from Spain, so let’s show you the custom content for your

location. Change

Select a country

In order to access the private area and corresponding sandbox, select the country of the APIs you want to use.